The rising cost of higher education in India has made financing a major concern for students and their families. Traditional bank loans often involve lengthy approval processes, high interest rates, and strict eligibility criteria. Enter fintech: a game-changer that is transforming the education loan landscape in India, making quality education more accessible and affordable than ever before.

Fintech companies are leveraging technology, data analytics, and innovative business models to streamline the loan application process, offer personalized financial solutions, and improve risk management. This has led to increased access to education financing, especially for students from marginalized communities.

Key Trends Shaping the Future of Education Loans in India:

Digital Lending Platforms: Fintech companies are providing online platforms that allow students to apply for loans quickly and easily, with minimal documentation.

AI-Powered Credit Underwriting: Artificial intelligence is being used to assess borrowers’ creditworthiness more accurately and efficiently, leading to faster loan approvals.

Account Aggregator Technology: This technology enables fintech companies to analyze a borrower’s financial data from multiple sources, resulting in better-informed lending decisions.

Personalized Loan Options: Fintech companies are offering customized loan terms and interest rates based on individual borrower profiles.

Financial Management Tools: These tools empower students to track their expenses and make informed financial decisions.

This article delves into the transformational impact of the fintech sector on education financing in India, with a focus on Novel Patterns, a leading SAAS fintech company that is shaping the industry.

Some data about the education loan sector in India with sources:

The education loan market in India is expected to reach USD 150 billion by 2025. (Source: CARE Ratings)

The market is currently dominated by public sector banks, but private banks and NBFCs are gaining market share. (Source: RBI Report: Sectoral Deployment of Credit)

The average education loan interest rate in India is around 10%. (Source: ClearTax)

The maximum loan amount that can be borrowed under the government’s education loan scheme is Rs. 7.5 lakh. (Source: MHRD)

Fintech companies are playing a growing role in the education loan sector by providing digital lending platforms and other services. (Source: Fintech India)

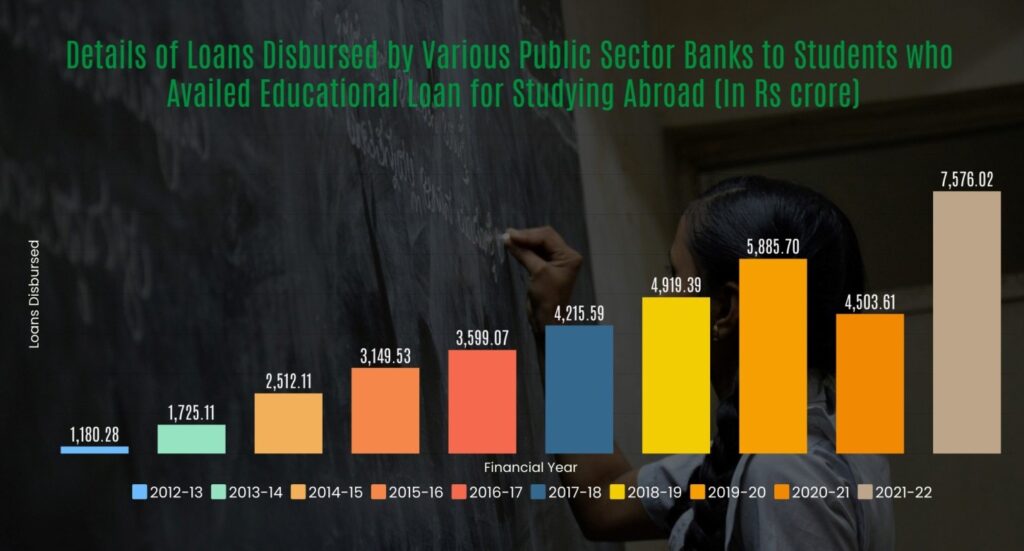

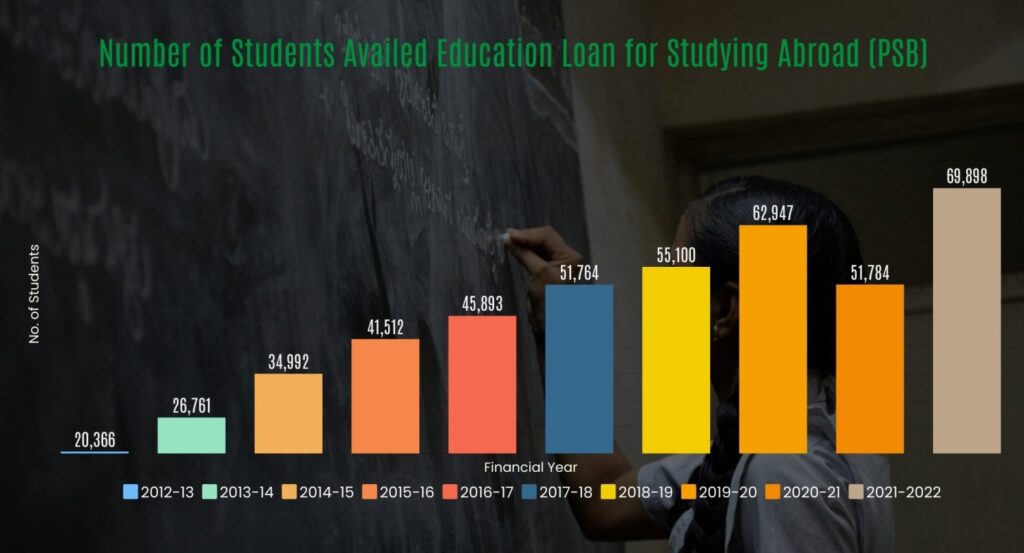

In response to a question raised in Lok Sabha on 13 February 2023, the Government of India provided information on the loans made available by PSBs for education abroad. The data is available for ten public sector banks (PSBs). According to these figures, around 4.61 lakh students received study-abroad loans from 2012-23 to 2021-22. This equals to Rs. 39.26 thousand crores in total. (Response in Lok Sabha -Unstarred Question 1759)

According to Public Sector Banks (PSBs), 4,61,017 students received educational loans to study overseas in the previous 10 years, with 42,364 receiving education loans to study medicine.

Details of loans disbursed by various Public Sector Banks to Students who availed Educational loans for studying abroad (In Rs crore)

Source: Response in Lok Sabha -Unstarred Question 1759

Number of students availed education loan for studying abroad (PSB)

Source: Response in Lok Sabha -Unstarred Question 1759

Here are some additional details about the education loan sector in India:

The demand for education loans is growing in India due to the rising cost of education.

The government has been providing financial assistance to students through education loans to help them access higher education.

Fintech companies are using technology to make the education loan process more efficient and accessible.

Another crucial role of fintech companies in education financing is the provision of software solutions that streamline operations and enable easier student onboarding for financial institutions and banks. Through advanced technologies such as credit underwriting platforms and video KYC (Know Your Customer) platforms, FinTech companies facilitate efficient loan origination, onboarding, disbursal, fraud detection, and customer service processes. These software solutions improve operational efficiency and enhance the overall borrower experience by automating and optimizing various aspects of the lending journey.

Additionally, fintech companies have introduced financial management tools that empower students to track their spending and manage their finances effectively. These solutions enable students to stay on top of their expenses, monitor budgets, and avoid accumulating debt. By providing insights and analytics, these tools assist students in making informed financial decisions and maintaining financial well-being throughout their educational journey.

The Need for Innovation in Education Financing

Education costs has been rising steadily, making it increasingly difficult for students from lower-income backgrounds to afford quality education without student loans in India. Traditional education financing options, such as bank loans, scholarships, and government grants, have proven inadequate in meeting the needs of aspiring students. Lengthy approval processes, high education loan interest rates, and the limited availability of credit have hindered the accessibility and affordability of education financing. This has led to a significant gap between the demand and supply of education financing in the country.

The rise of fintech companies in India has brought about a paradigm shift in the way education financing is perceived and accessed. By leveraging technology, data analytics and innovative business models, fintech firms are revolutionizing the education financing landscape in the following ways:

Streamlined Student Loan Origination and Approval: Fintech companies are introducing automated processes and advanced algorithms to streamline the loan origination and approval process. By utilizing big data and machine learning, these platforms can assess the creditworthiness of applicants more accurately and efficiently. This not only reduces the time required for loan approvals but also increases the accessibility of education financing to a broader population.

Enhanced Transparency and Accessibility: Fintech platforms are leveraging technology to provide transparent and user-friendly interfaces that simplify the application and disbursement processes. Through online portals and mobile applications, students and their families can access detailed information about available financing options, interest rates, repayment terms, and eligibility criteria. This increased transparency fosters trust and empowers borrowers to make informed decisions about their education financing.

Personalized Financial Solutions: Fintech companies are employing data analytics to develop personalized financial solutions tailored to the specific needs of students. By considering factors such as academic performance, career prospects, and income potential, these platforms can offer customized loan terms, repayment plans and interest rates. This approach ensures that students receive financing options that align with their individual circumstances and significantly reduce the burden of loan repayment.

Integration of Account Aggregation Technology: Account aggregation technology allows fintech platforms to securely access and analyze an individual’s financial data from multiple sources. By incorporating this technology into their offerings, fintech companies can assess an applicant’s financial health more comprehensively, leading to better-informed lending decisions. This integration also facilitates the verification of income, assets, and financial commitments, further improving the accuracy of credit assessments.

Overall, the innovative approaches adopted by fintech companies have the potential to bridge the gap between the demand and supply of education financing in India. By leveraging technology, data analytics and personalized financial solutions, these firms are making education financing more accessible, transparent and tailored to the needs of students. This transformation in the education financing landscape holds promise for enabling more individuals, particularly those from lower-income backgrounds, to pursue quality education and achieve their academic aspirations.

In India, the execution of an education loan involves several stages, starting from loan sourcing to disbursal. Throughout the process, credit underwriting plays a crucial role in assessing the borrower’s creditworthiness. Additionally, fintech software and technology are often employed to streamline the loan application, verification and disbursement processes. Here’s an overview of how the education loan process typically unfolds:

Loan Sourcing: The borrower, typically a student or their parent/guardian, initiates the loan application process by approaching a bank or a fintech lending platform that offers education loans. They provide the necessary details and express their interest in availing of a loan for educational purposes.

Application Submission: The borrower fills out the loan application form, either online or offline, and submits it along with the required documents. These documents usually include proof of identity, address, income, academic records, an admission letter, the fee structure and any collateral documentation if applicable.

Credit Underwriting: The lending institution, whether a bank or a fintech platform, performs credit underwriting to evaluate the borrower’s creditworthiness and ability to repay the loan. This process involves assessing various factors such as the borrower’s income, credit history, academic performance and potential career prospects.

Document Verification: The lending institution verifies the authenticity and accuracy of the submitted documents. This involves scrutinizing academic records, income certificates, identity proofs and other relevant documents. Fintech software can be used to automate and streamline this verification process, reducing the time required for document checks.

Loan Approval: Based on the credit underwriting assessment and document verification, the lending institution decides whether to approve or reject the loan application. If approved, the terms and conditions of the loan, including the loan amount, interest rate, repayment tenure and any applicable fees, are communicated to the borrower.

Loan Disbursal: Once the loan is approved, the lending institution initiates the disbursal of funds to the borrower or directly to the educational institution. Fintech platforms often facilitate quick and secure disbursals through electronic fund transfers or other digital payment methods.

Repayment:After the loan is disbursed, the borrower must start repaying the loan according to the agreed-upon terms and conditions. The repayment period may vary depending on the lender’s policies and the borrower’s financial situation. The borrower is typically expected to make monthly or quarterly payments towards the loan principal and interest.

Also, Within the realm of education financing in India, some of the Education loan organizations like Eduvanz and Avanse are providing students with low-interest loans and expediting the loan approval process.

Eduvanz, renowned as a low-interest education loan provider, has been instrumental in enabling students to pursue their educational aspirations without the burden of exorbitant interest rates. Their innovative approach aims to make education financing affordable and accessible to students from all backgrounds. By leveraging advanced technology and data analytics, Eduvanz offers customized loan solutions tailored to individual needs, ensuring that students can finance their education without compromising their financial well-being. With flexible repayment options and competitive interest rates, Eduvanz has become a beacon of hope for countless students across the country, transforming their dreams into reality.

Avanse, on the other hand, has carved a niche for itself by providing the fastest sanction within 72 hours for education loans. Recognizing the urgency and time sensitivity associated with education financing, Avanse has streamlined its loan approval process, ensuring quick disbursal of funds to deserving students. By leveraging technology, Avanse has optimized its operations, eliminating unnecessary delays and bureaucratic hurdles that often hinder the loan approval process. This swift and efficient approach has proven to be a game-changer for students, allowing them to focus on their education rather than worrying about financial intricacies.

Throughout this process, fintech software and technology play significant roles in streamlining and enhancing efficiency. They facilitate online loan applications, automate document verification, enable digital communication, and accelerate the disbursal process. Fintech platforms often leverage data analytics, machine learning and account aggregation technology to assess creditworthiness, provide personalized loan options, and offer transparent and user-friendly interfaces for borrowers.

In summary, the education loan process in India involves loan sourcing, application submission, credit underwriting, document verification, loan approval, disbursal, and repayment. Credit underwriting assesses the borrower’s creditworthiness, while fintech software streamlines the process, automates document checks, and enhances the efficiency of loan sourcing, verification and disbursement stages.

Novel Patterns: Transforming Education Financing in India

www.novelpatterns.com

As a SAAS fintech company, Novel Patterns specializes in providing a streamlined setup of operations for financial institutions and banks, enabling them to improve their lending processes within the education sector. The company offers two flagship products to transform the lending ecosystem in India:

CART is a robust AI-driven credit underwriting platform that leverages advanced data analytics, machine learning algorithms and account aggregation technology. It enables financial institutions and banks to make data-driven lending decisions with enhanced accuracy and efficiency. CART’s integration with account aggregation enables lenders to gather comprehensive financial information, enabling them to assess creditworthiness more accurately. This empowers lenders to offer suitable financing options to students and optimize risk management.

A Video Engagement Platform for Video KYC & Personal Discussion Solution

MyConCall is a secure video KYC (Know Your Customer) and personal discussion platform by Novel Patterns. This platform eliminates the need for physical document verification, allowing financial institutions to conduct KYC processes remotely. By enabling virtual face-to-face interactions between lenders and borrowers, MyConCall enhances the onboarding experience, reduces turnaround time and improves customer satisfaction. This platform ensures compliance with regulatory requirements while enabling efficient and secure customer onboarding.

Impact and Benefits

The fintech revolution in education financing, driven by companies like Novel Patterns, has brought numerous benefits to the education ecosystem in India:

Increased Accessibility: Fintech platforms have widened access to education financing, especially for students from marginalized communities or with limited financial means. The simplified application processes, personalized loan offerings, and reduced processing times have made education financing more accessible and inclusive.

Improved Efficiency: The integration of advanced technology, data analytics, and automation has significantly improved the efficiency of education financing operations. Fintech platforms have reduced the time and effort required for loan approvals, disbursals, and customer service, enhancing the overall borrower experience.

Enhanced Risk Management: Fintech companies leverage data analytics and account aggregation technology to assess creditworthiness accurately. This results in improved risk management practices for lenders, reducing the likelihood of defaults and ensuring the sustainability of education financing programs.

Empowered Decision Making: Students and their families now have access to comprehensive information about education financing options, interest rates and repayment terms. This transparency empowers borrowers to make informed decisions and choose the most suitable financing options for their educational aspirations.

Through these innovative products, Novel Patterns is not only accelerating the growth of fintech solutions in the education loan sector but also contributing to the accessibility, customization, and efficiency of education financing in India. As we embrace these advancements, we pave the way for a future where education becomes truly accessible to all, empowering students to fulfill their academic aspirations and shape a brighter tomorrow.

Rewind-Up

The fintech sector has revolutionized education financing in India, addressing the limitations of traditional methods and opening up new possibilities for students to pursue their educational goals.

Through streamlined processes, increased accessibility, personalized financial solutions, and enhanced risk management, fintech companies have transformed the education financing landscape. Companies like Novel Patterns, with their innovative products like CART and MyConCall, are leading the way in reshaping the lending ecosystem, ultimately making quality education more affordable and accessible to all.As India continues to embrace digital transformation, the fintech sector’s role in education financing is expected to grow further, empowering generations to come. Moreover, the use of artificial intelligence and machine learning algorithms has enabled fintech companies to assess the creditworthiness of borrowers more accurately and efficiently. This has resulted in a reduction in default rates and increased access to financing for students from all socioeconomic backgrounds. With these advancements, the future of education financing looks promising as fintech companies continue to drive innovation in this space.

Empower your financial journey with Novel Patterns, where cutting-edge technology meets tailored solutions.

Elevate your business with our innovative Fintech SaaS offerings.

Contact us today to discover the future of finance.